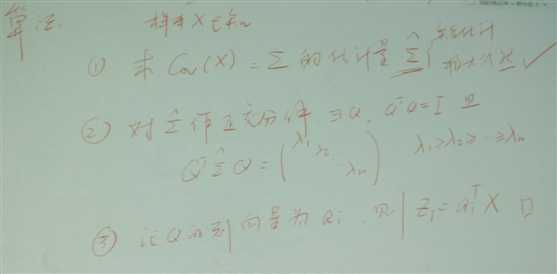

超高维度分析,N*P的矩阵,N为样本个数,P为指标,N<<P

PCA:抓住对y对重要的影响因素

主要有三种:PCA,因子分析,回归方程+惩罚函数(如LASSO)

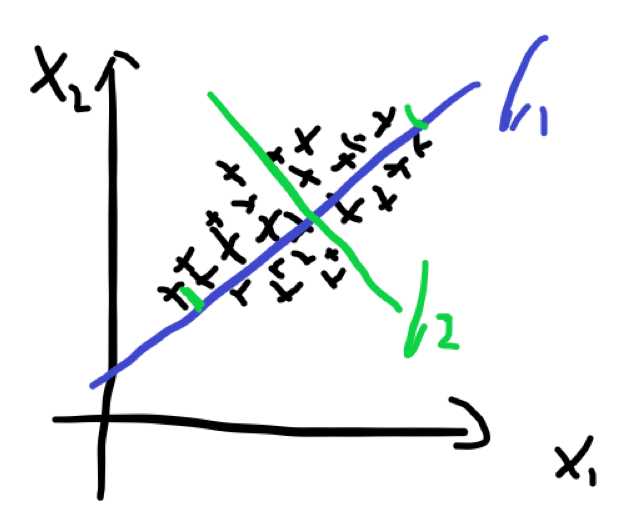

为了降维,用更少的变量解决问题,如果是二维的,那么就是找到一条线,要使这些点再线上的投影最大,投影最大,就是越分散,就考虑方差最大。

> conomy<-data.frame(

+ x1=c(149.3, 161.2, 171.5, 175.5, 180.8, 190.7,

+ 202.1, 212.4, 226.1, 231.9, 239.0),

+ x2=c(4.2, 4.1, 3.1, 3.1, 1.1, 2.2, 2.1, 5.6, 5.0, 5.1, 0.7),

+ x3=c(108.1, 114.8, 123.2, 126.9, 132.1, 137.7,

+ 146.0, 154.1, 162.3, 164.3, 167.6),

+ y=c(15.9, 16.4, 19.0, 19.1, 18.8, 20.4, 22.7,

+ 26.5, 28.1, 27.6, 26.3)

+ )

> #### 作线性回归

> lm.sol<-lm(y~x1+x2+x3, data=conomy)

> summary(lm.sol)

Call:

lm(formula = y ~ x1 + x2 + x3, data = conomy)

Residuals:

Min 1Q Median 3Q Max

-0.52367 -0.38953 0.05424 0.22644 0.78313

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -10.12799 1.21216 -8.355 6.9e-05 ***

x1 -0.05140 0.07028 -0.731 0.488344

x2 0.58695 0.09462 6.203 0.000444 ***

x3 0.28685 0.10221 2.807 0.026277 *

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.4889 on 7 degrees of freedom

Multiple R-squared: 0.9919, Adjusted R-squared: 0.9884

F-statistic: 285.6 on 3 and 7 DF, p-value: 1.112e-07

> #### 作主成分分析

> conomy.pr<-princomp(~x1+x2+x3, data=conomy, cor=T)

> summary(conomy.pr, loadings=TRUE)

Importance of components:

Comp.1 Comp.2 Comp.3

Standard deviation 1.413915 0.9990767 0.0518737839

Proportion of Variance 0.666385 0.3327181 0.0008969632

Cumulative Proportion 0.666385 0.9991030 1.0000000000

Loadings:

Comp.1 Comp.2 Comp.3

x1 0.706 0.707

x2 -0.999

x3 0.707 -0.707

> #### 预测测样本主成分, 并作主成分分析

> pre<-predict(conomy.pr)

> conomy$z1<-pre[,1]

> conomy$z2<-pre[,2]

> lm.sol<-lm(y~z1+z2, data=conomy)

> summary(lm.sol)

Call:

lm(formula = y ~ z1 + z2, data = conomy)

Residuals:

Min 1Q Median 3Q Max

-0.89838 -0.26050 0.08435 0.35677 0.66863

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 21.8909 0.1658 132.006 1.21e-14 ***

z1 2.9892 0.1173 25.486 6.02e-09 ***

z2 -0.8288 0.1660 -4.993 0.00106 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.55 on 8 degrees of freedom

Multiple R-squared: 0.9883, Adjusted R-squared: 0.9853

F-statistic: 337.2 on 2 and 8 DF, p-value: 1.888e-08

> #### 作变换, 得到原坐标下的关系表达式

> beta<-coef(lm.sol); A<-loadings(conomy.pr)

> x.bar<-conomy.pr$center; x.sd<-conomy.pr$scale

> coef<-(beta[2]*A[,1]+ beta[3]*A[,2])/x.sd

> beta0 <- beta[1]- sum(x.bar * coef)

> c(beta0, coef)

(Intercept) x1 x2 x3

-9.13010782 0.07277981 0.60922012 0.10625939

原文:https://www.cnblogs.com/caiyishuai/p/11169073.html